At a glance

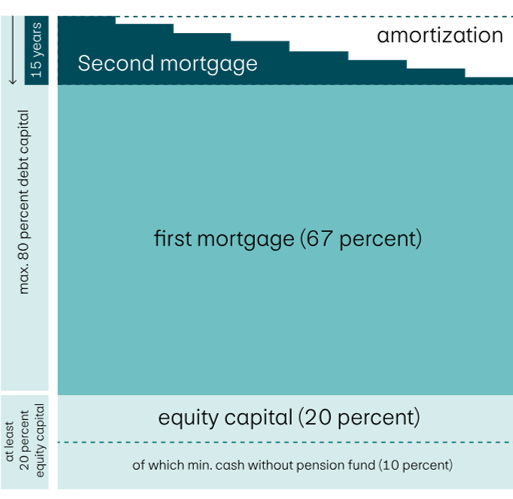

- In Switzerland, only the second mortgage generally has to be amortized. It must be repaid within 15 years or by the time you retire at the latest.

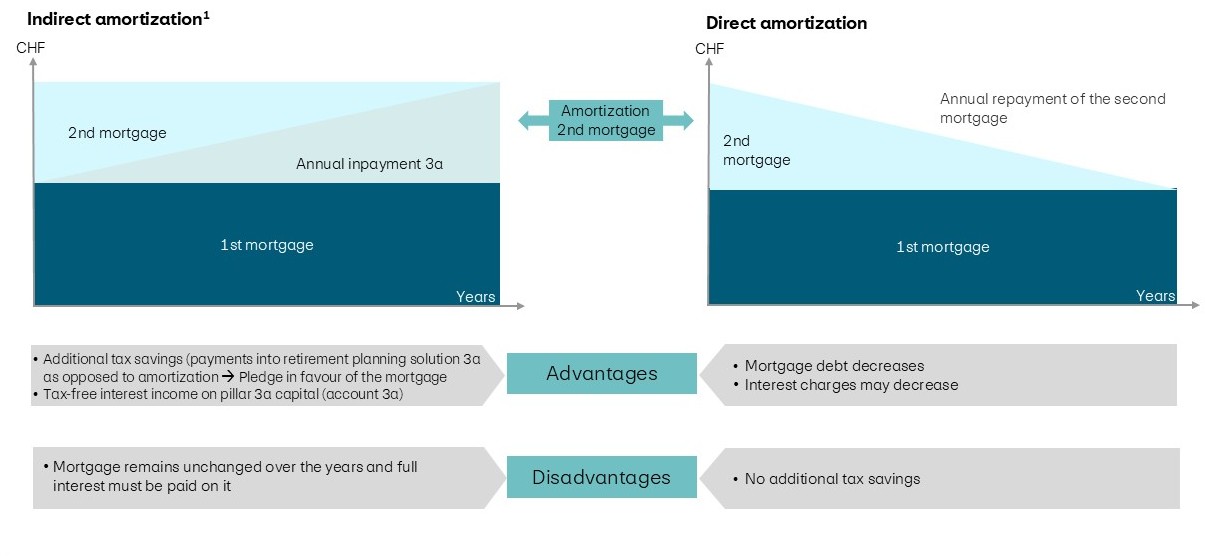

- With direct amortization, you continuously reduce your mortgage debt. This lowers your interest costs, while at the same time reducing your tax deductions.

- With indirect amortization, you pay into a pledged retirement planning solution. The mortgage remains in place, but you can benefit from tax advantages.

- The type of amortization that makes sense depends on factors including income, assets, tax situation, investment behaviour and personal preferences.

Not sure which type of amortization is right for your situation? Our mortgage advisors will help you find the right financing solution and comprehensively assess tax and financial aspects.