This page has an average rating of %r out of 5 stars based on a total of %t ratings

Reading Time 5 Minutes

Reading Time 5 Minutes

What are barrier reverse convertibles?

19.10.2022

In markets with few fluctuations, just gently rising or slightly falling trends or sustained low interest rates, many investors ask themselves the same question: how do I generate a yield at an acceptable level of risk? One possible answer is barrier reverse convertibles. But what are these and how can I use them to generate a yield? This article will tell you everything you need to know.

What are barrier reverse convertibles?

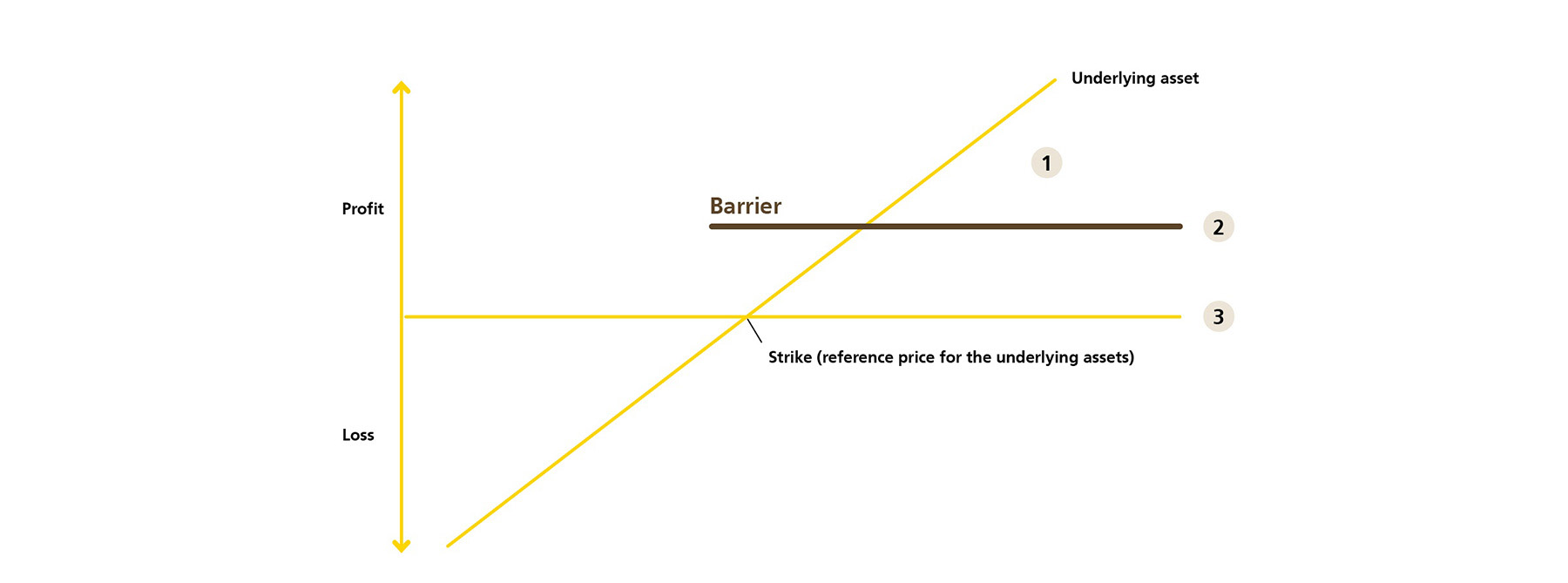

Essentially, these are “equity-like bonds” but are not necessarily just share-type products. For example, barrier reverse convertibles are also traded on precious metals and raw materials. They are a structured financial product, comprised of a bond and a put option . This results in a certificate with what’s known as a “barrier”. This refers to an agreed threshold that the price of the underlying base value should not reach or even fall below throughout the entire term or on a certain day because otherwise investors usually suffer a loss.

1) No barrier event up to end of term: 100% denomination and coupon

2) Barrier event took place, but not at the end of the term: a. European barrier: 100% denomination and coupon if the event does not fall at the end of the term. b. American barrier: Either 100% denomination and coupon or denomination with reduction of 1% in each case, delivery of underlying asset or cash settlement.

3) Barrier event at the end of the term: same scenario as per point 2) American barrier

A barrier reverse convertible is a combination of a bearer bond – a security with which the issuer undertakes to provide a benefit – and a special put option on a classic financial asset, such as shares or raw materials. The financial asset is designated as the base value. During the term, a barrier reverse convertible grants a predefined coupon , regardless of how the base value develops. The maximum return from this type of product is therefore limited to the coupon.

The repayment on expiry, however, depends on the base value development (e.g. shares). What matters is whether the price of a base value has traded at or under the specified barrier during the term or at the agreed observation point. If the barrier reverse convertible includes several base values, the “worst of” principle typically applies. In other words, the relevant base value with the worst development is used to determine the repayment amount – regardless of whether this has fallen below the barrier. Because of the higher risk involved with several base values, these products generally offer a more attractive coupon than products with just one base value. This means that investors in barrier reserve convertibles primarily bear the market risk of the underlying base value. This makes barrier reverse convertibles most popular in stagnating markets.

However, barrier reverse convertibles can work in different ways. The rules that apply to reaching or falling below the barrier and the subsequent repayment depend on the type of barrier.

Which barrier types are there?

Depending on the barrier type and its construction, the development of the base value is observed differently. The two most common barrier types are:

European barriers

The European barrier type is checked only at the end of the term to see whether the base value is at or below the barrier. How the price has developed through the whole term has no effect on the repayment scenario.

American barriers

With the American barrier type, the price of the base value is observed continually. This means that throughout the entire term, checks are made as to whether the base value is at or below the barrier.

Which repayment scenarios can be triggered?

Generally, with “classic” barrier reverse convertibles – i.e. barrier reverse convertibles without an early repayment option – three different scenarios are possible:

Scenario 1: No barrier event took place before the end of the term

No barrier event took place because the market price of the base value was neither at nor below the specified barrier in the defined time period. In this case, the investor receives 100% of the coupon. There is no difference here between the European and American variants.

Scenario 2: During the term, a barrier event took place but not at the end of the term

This scenario varies depending on the type of barrier:

European barriers: the reference date for European barriers is the end of the term. If a barrier event took place, but not right at the end of the term, the investor receives repayment of 100% of the denomination and the coupon.

American barriers: all days in the entire term are reference dates for American barriers. If at least one base value traded at or below the barrier during the term, but at the end of the term the base value with the worst price development is above the initial fixing, the investor will also be paid 100% of the denomination and the coupon. However, if at least one base value trades at or below the barrier during the term, and at the end of the term the base value with the worst price development is at or below the initial fixing, the investor will be paid the denomination less 1% for each percent of negative development of the base value with the worst price development starting from the initial fixing. Where there are several base values, the “worst of” principle mentioned above applies – the repayment amount is determined from the base value with the worst development. Repayment can be made either through delivery of the base value or via a cash payment equivalent to the development of the base value. This depends on the structure of the relevant product. If fractions arise in the context of repayments, i.e. fractional shares, these are compensated in cash. Naturally, the investor also receives the agreed coupon here too.

Scenario 3: A barrier event took place at the end of the term

For both barrier types, a barrier event at the end of the term means the same thing: a barrier event has taken place on a reference date and the repayment scenario is exactly the same as with an American barrier in Scenario 2.

Details of the applicable repayment scenarios can be found on the relevant barrier reverse convertibles term sheet. More information on the individual scenarios can also be found in the “The link will open in a new window Structured products” brochure from PostFinance.

Barrier reverse convertibles with early repayment options

While the scenarios above apply to classic barrier reverse convertibles, the scenarios for products known as “callable” barrier reverse convertibles are slightly different. The reason for this is that issuers can decide for example with soft callable products on stipulated references dates whether they will repay the product early in accordance with the denomination with the respective share of the coupon. If the issuer repays the coupon early, the investor receives 100% of the denomination in addition to the accrued coupon. Autocallable products work in a similar way but with these, the preconditions for early repayment of the product are defined when the product is launched. In the case of early repayment, the investor also receives 100% of the denomination in addition to the accrued coupon.

Higher potential returns make barrier reverse convertibles attractive

At low interest rates, stagnating or only slightly rising or falling share markets are often unattractive to direct investors in shares. With shares, investors only benefit when prices rise or when dividends are distributed.

In this environment, the attractiveness of barrier reverse convertibles lies in the guaranteed coupon, which is paid out regularly. This means that, with the coupon, an excess return on a direct investment in shares can be generated when the price of the base value is stagnating.

Don’t lose sight of the risk, even with barrier reverse convertibles

This attractive aspect of barrier reverse convertibles is likewise linked with risks. When prices rise significantly, direct investments in shares have an advantage over barrier reverse convertibles, the returns of which are restricted to the coupon. If, at the end of the term, the price of the base value is higher than the initial price, the investor still recovers only the initial investment amount and the coupon. Investors do not benefit from price gains or any potential dividend distributions from the base value.

When prices are falling, the contingent capital protection likewise falls away if the price of the base value reaches or is below the agreed barrier during the term.

It’s not just about the coupon

Investors must also consider that, at the end of the term and in the case of a barrier event, securities are paid into the custody account. When you invest, you should therefore weigh up whether you want to bear any market risks arising from the base value before investing in barrier reverse convertibles. Concentrating solely on the potentially attractive coupon would be too one-sided. You should also consider the issuer risk and/or the creditworthiness of the issuer. This can be achieved firstly by selecting products from a variety of issuers. Secondly, the risk can be reduced by deliberately selecting products from an issuer with a good credit standing.

Unlike investment funds, barrier reverse convertibles and structured products in general are not regarded as segregated assets. If the issuer were to go bankrupt, the capital invested in barrier reverse convertibles would therefore not be protected. We therefore advise you not to underestimate the choice of issuer.

Which investors are barrier reverse convertibles suitable for?

In general, barrier reverse convertibles are suitable for investors who are familiar with structured products and expect the base value to experience stagnation or a slightly rising or falling price. Anyone who wants to invest in this type of structured product should also consider whether the underlying base value (e.g. shares) would suit their portfolio . If these preconditions are met, barrier reverse convertibles represent an attractive yield enhancement opportunity in stagnating markets.

Points to consider with barrier reverse convertibles

Get to know the different types and scenarios of barrier reverse convertibles.

Be aware that barrier reverse convertibles can be attractive primarily in stagnating markets.

Don’t be blinded by an attractive coupon: you may be left at the end of the term with shares that have fallen sharply in value.

This page has an average rating of %r out of 5 stars based on a total of %t ratings

Rate this article

Your feedback is important to us.

Your input will help us to continuously optimise our platform. Your feedback will not be published.